Coffee Stain $COFFEE.B-ST

Coffee Stain at single-digit Cash EBIT with an inflection point

Disclaimer: this is a direct translation from the original post from beginning of march from Swedish to English using AI where it has been instructed to not rewrite anything and keep the original wording.

Single-digit cash multiple with high margin and upcoming inflection points

Coffee Stain is effectively being traded like a mobile gaming company with uncertain future and high investments, where the market appears to be pricing in that the catalogue is rolling over and that today’s cash flow is near a peak. What looks like growing fundamental distrust in the share price is to a large extent explained by other things: technical flows following the spin-off, heavy dollar exposure where analyst forecasts are built on higher dollar levels than the market is pricing in, and misunderstandings of the business model combined with overly simplified interpretations of player KPIs, including on Steam.

A different reading of the data points more towards a normalisation after a previous peak, a temporarily delayed cadence of expansions, and currency effects, rather than weak underlying demand. At the same time, the company trades at a single-digit cash flow multiple on the current year, despite several near-term triggers with good visibility and optionality to drive growth beyond the next twelve months. With a strong net cash position and a clean balance sheet, the question is whether the market, through flows and lack of track record has priced in the ending when in reality it has the potential to keep paying out a high yield for an extended period.

The thesis breaks down if the catalogue actually rolls over, which would show up as weak activity despite new releases and following price discounts. If upcoming releases are delayed, receive a lukewarm reception, or if the currency moves further in the wrong direction, a big chunk of the growth falls away. The stock can also continue trading at a discount for longer than expected due to its size, unregulated marketplace, and a potentially unprofilied shareholder base.

Things that could act as catalysts for Coffee Stain in the near term include the market gradually gaining visibility on the durability and normalised release cadence, confidence in growth initiatives. Capital allocation plans, whether through dividends, buybacks in the future once those are permitted, or potential M&A. And communication around financial targets on a short or medium-term horizon, which today are conspicuously absent and prevent market participants from drawing lines further out.

The initial scare

There’s a particular phase in a stock’s decline when the numbers stop being enough. When the price keeps falling, the market starts searching for explanations. Is it fund flows, old Embracer holders cleaning up their portfolios after the Coffee Stain spin-off, or something more uncomfortable slowly creeping to the surface? Probably a familiar feeling for many small-cap holders these past quarters.

For Coffee Stain there’s reason to start with the shareholder register rather than the drama. The stock has fallen around 30 percent this year but a good deal suggests that a larger part of the pressure has been technical. When the company landed on the small First North list, holdings were forced out of portfolios with mandates that don’t allow an unregulated marketplace along with size restrictions. Before year-end, around 36 percent of the shares were traded. 19 percent of those are identified in the tables below. Since then up until beginning of march, an additional roughly 25 percent of the share capital has changed hands. After year-end, institutional movements likely followed tied to the restructuring of the AP funds which are giant institutional behemoths packing thousands of billions in assets under management. Where AP1’s holding of approximately 4.4 percent may have become yet another part of the flow pressing the stock when those shares moved to AP3 and AP4 and triggered unconstrained selling.

Each individual sale can be explained rationally. But together they become a selling pressure that doesn’t necessarily say much about the actual business. And that’s where the market often goes astray, because flows and technicals come across as harsh verdicts on fundamentals.

It’s troublesome because Coffee Stain was long seen as one of Embracer’s clearest crown jewels. Ahead of the spin-off, a company valuation around SEK 7 billion was talked about. Today the enterprise value is just above SEK 3 billion including their net cash position. At the spin-off, the valuation didn’t look particularly stretched. Around 15 times current-year operating profit was more in line with what the market often pays for a gaming company with strong titles, long revenue tails, and recurring cash flows.

The problem that’s been brought to the fore is that the gaming industry as a whole rarely delivers in straight lines. New titles, delays, and reception make profits uneven. Everyone knows this in theory, yet the market often behaves as if every dip were a new surprise. The cyclical swings are something you as an investor need to dare to exploit. The question in Coffee Stain is therefore not just how the games are performing, but whether the share price decline has led the market to read in a fundamental problem, that the tail on the games is dying.

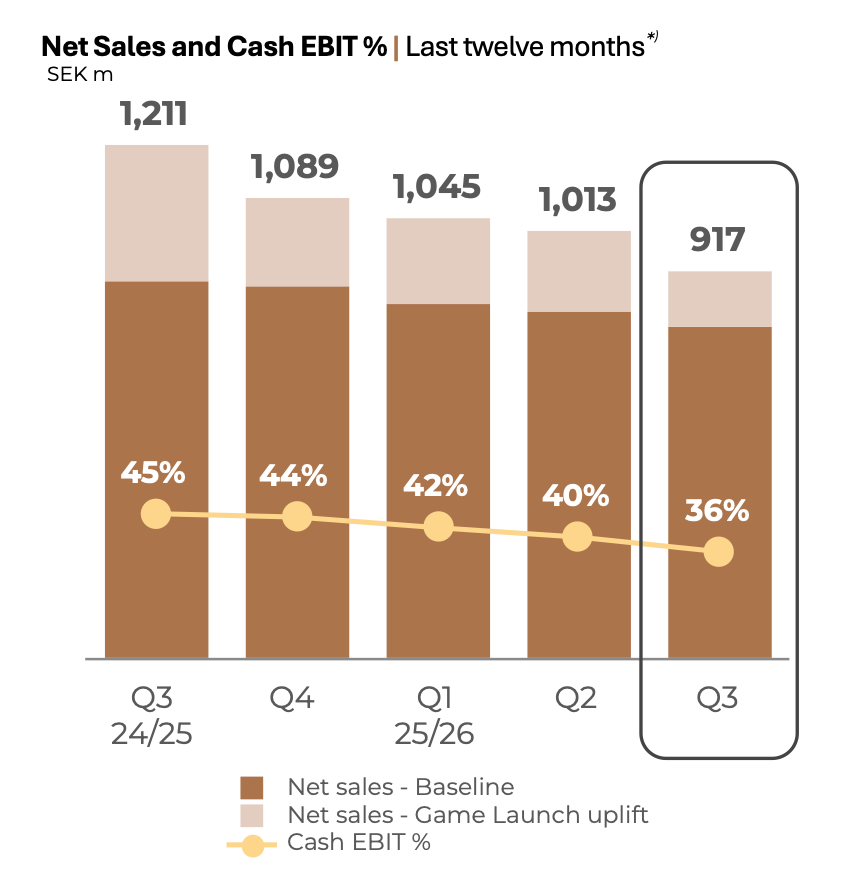

Because that’s what you’re led to believe when you look at the latest report from the company where they present earnings on a rolling twelve basis. And so the uncertainty grows in the potential investor: is the stock falling because the market distrusts the company, or does the market distrust the company because the stock is falling?

The mines of gaming companies

Gaming companies are often described as creative workshops or mines. And sure, there’s something appealing about that image. Teams building worlds, polishing ideas, and hoping to strike gold in an industry where imagination can be turned into cash flow. But it’s also an image that risks concealing an important distinction, that not all gaming companies operate on the same logic. Not everyone is digging for the same kind of deposit in their mine.

At one end you find studios that bet everything on singular big launches. Games are developed over three to five years, often with large teams and significant risk. If they don’t get scrapped in the process. The idea is simple but brutal: when the game finally ships it needs to sell many millions of copies in a short time where a lot is decided. Where something as simple as review-bombing can destroy the discoverability and thereby the distribution of a game during a few critical days. If the game lands right, it can be followed by expansions and a longer life. If it misses expectations, there’s rarely much to hide behind. Revenues become cyclical and the wait between these periods gets very long.

At the other end you find gaming companies with a different rhythm to their business. The launch isn’t the endpoint but merely a beginning. These games are built to live for a long time, sometimes many years, with a constant flow of content, expansions, and updates. Several additions per year is not uncommon. Players stick around, invest time, learn the systems, and make the game a habit rather than a one-time experience. When that model works, the relationship with the customer becomes one where they keep coming back for more. Hundreds of hours played becomes the rule rather than the exception, and that’s the most valuable asset in the sector today and what every company is fighting over. The players’ time. Someone who’s already spending evenings, weekends, and has friends they play with often has less room for others. It’s in that category of companies that Coffee Stain and Paradox Interactive are often placed.

This is where some investors wonder whether there’s any future growth in Coffee Stain. But in reality most successful games and gaming companies today have only a handful of titles they commit to over a long period. That’s also the answer CEO Anton gives when investors ask, and it’s visible in the company’s own allocation where roughly 80% of development goes to existing games and 20% to new ones.

Part of what looks fundamental with declining revenue has a considerably more boring explanation. When 95 percent of revenues come in dollars, a 15% weakening of the currency since the 2024 peak hits the reported top line hard. Adjusted for that effect, it’s difficult to see any clear decline.

Is the catalogue rolling over or just normalising?

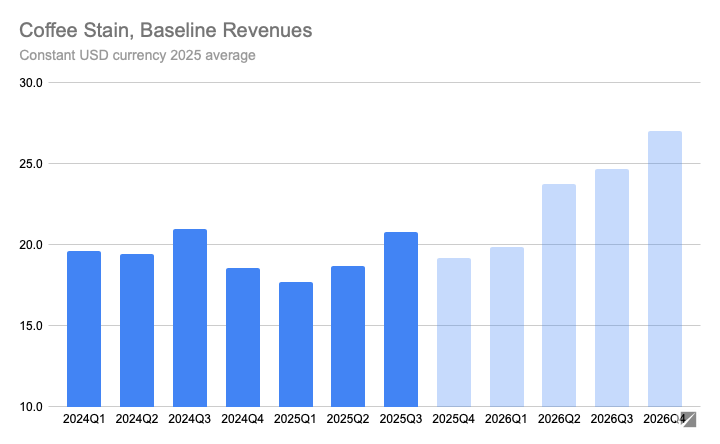

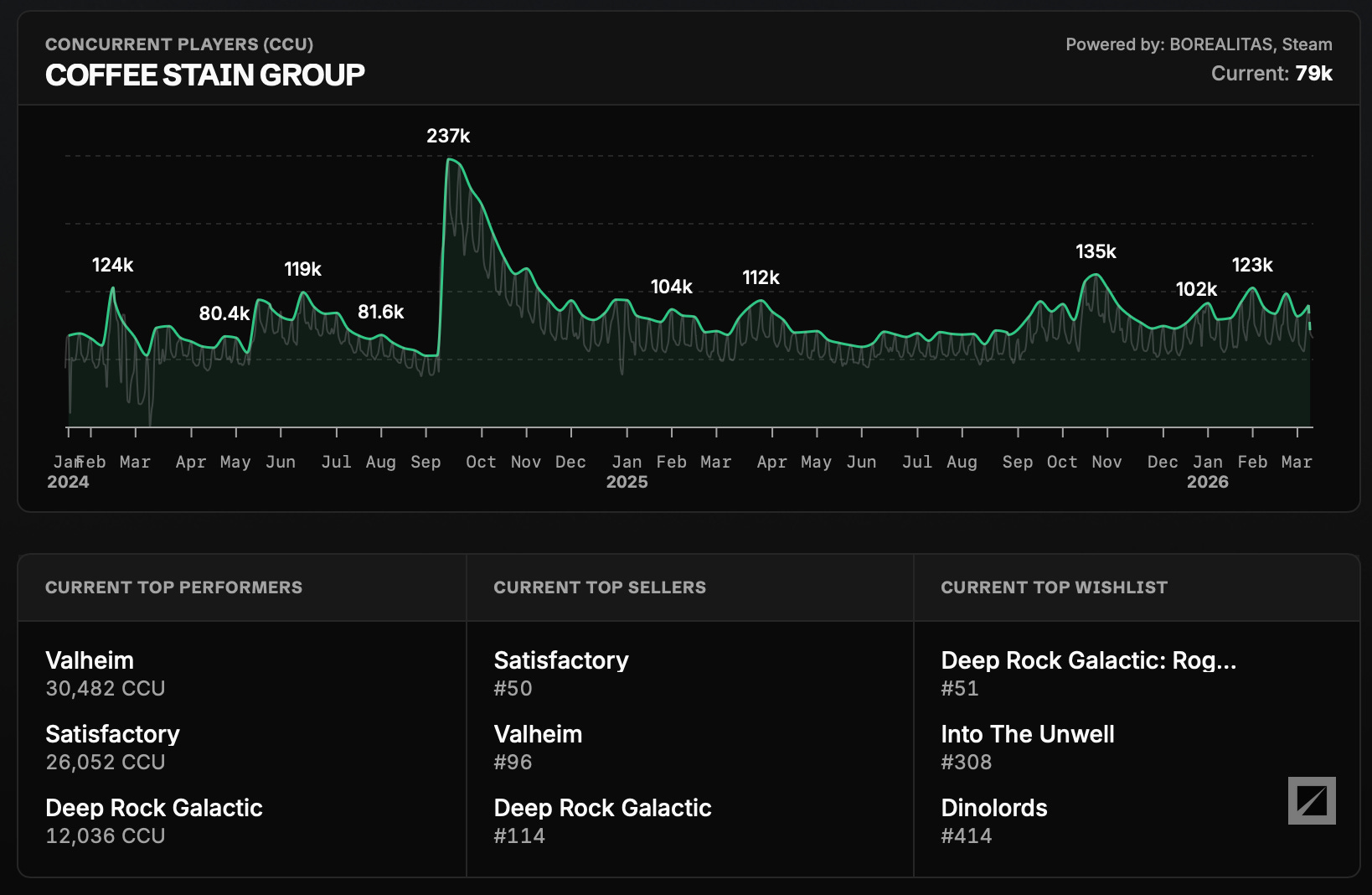

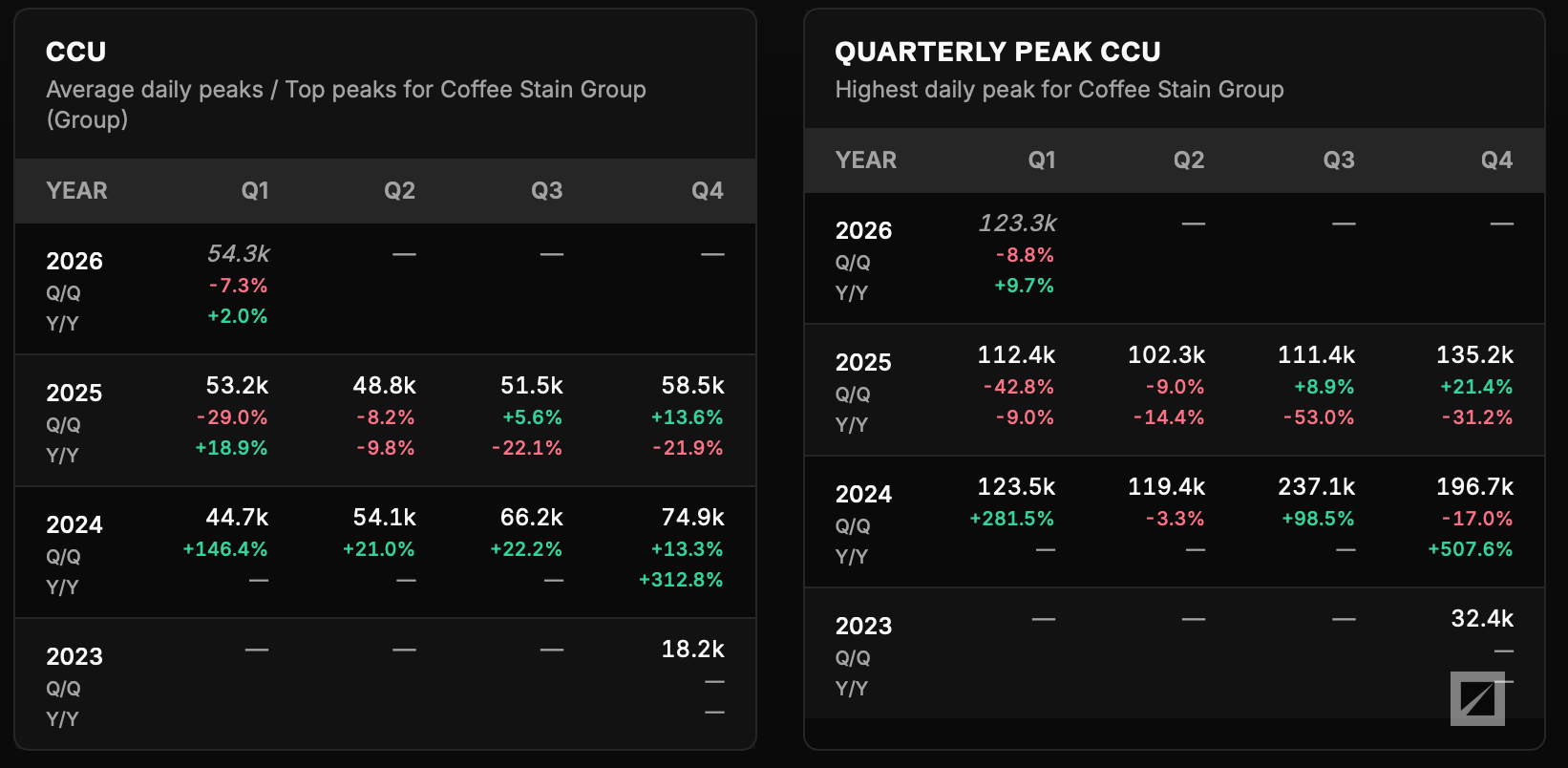

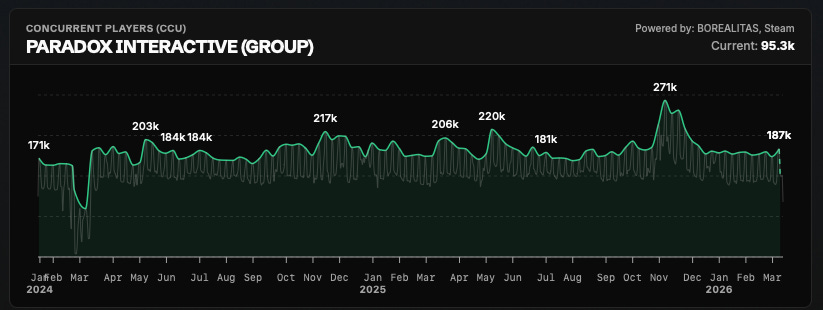

One of the other objections that have surfaced around Coffee Stain as the stock has headed lower is that parts of the game portfolio resemble mobile games. Not just in how the market values it, but also how the games are perceived. The thesis is partly based on a Kepler analysis from early March arguing that player counts have fallen sharply after a peak in 2024 and that the portfolio lifecycle is now rapidly fading out. From there it wasn’t far to the conclusion that there are no material catalysts that could turn sentiment. Kepler’s interpretation rests on “annualising” the player count on the PC platform Steam and comparing the player count in January 2026 with each game’s peak, something that’s a bit hard to follow the reasoning behind. Instead, I’d say an aggregated picture instead better shows the overall development.

During 2024 Satisfactory left its Early Access stage and was released as version 1.0. With that it reached 237 thousand concurrent players on Steam. A number it hasn’t managed to beat since. But that’s a natural part of how Live Ops games on Steam work over time, with visibility, player flows, and commercial weight shifting. And an important piece in how you continuously use price discounts to drive new players in. Kepler’s analysis therefore misses the fact that they’ve held a steady player count on Steam after Satisfactory normalised and have remained consistently on the sales charts.

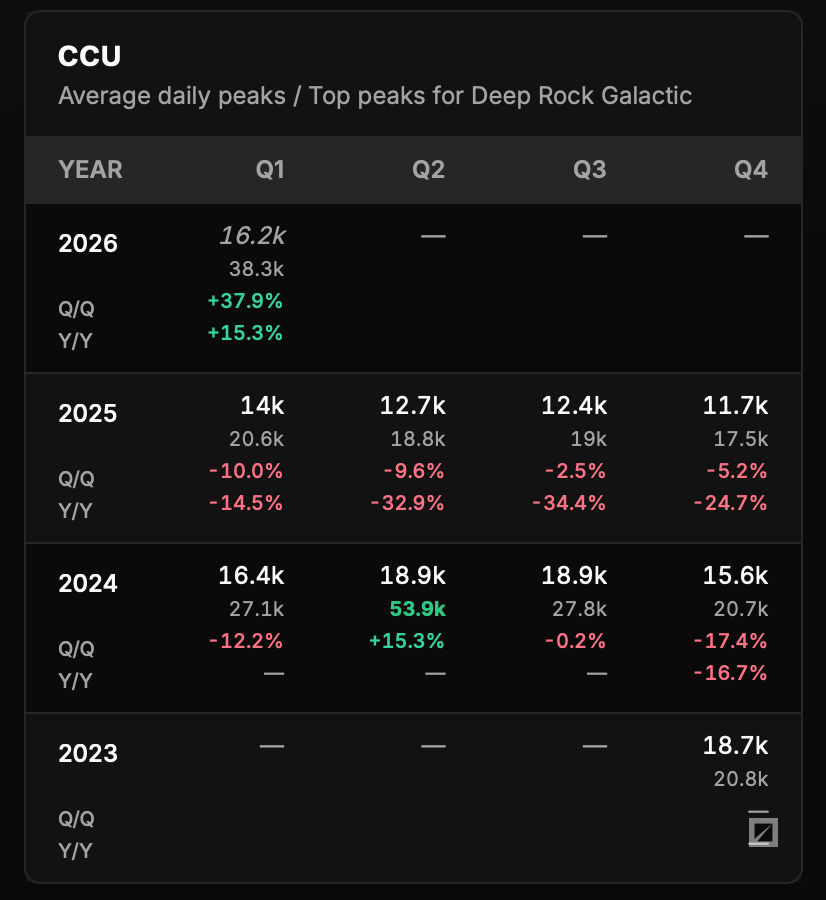

From that perspective it’s therefore difficult to see a broad and unambiguously declining trend in Coffee Stain’s game portfolio on PC. But there’s one clear exception in Deep Rock Galactic, which showed declining sequential CCU development for six straight quarters after the launch of season five in Q2 2024. For an “always-online” audience, this is an eternity without updates. But even there, there’s a more tangible explanation than players or the studio having lost interest. The Danish studio Ghost Ship Games simultaneously put all its resources on the sequel Deep Rock Galactic: Rogue Core, which meant season six was delayed a full seven quarters. To get the new season in place, they ultimately chose last year to move the season’s development to sister studio Invisible Walls. When the season launched in the current quarter, it drove back a large number of players and sales.

This is important in context because Coffee Stain’s games are rarely just about sales at launch but about the ability to keep a player base active and satisfied over time. That’s where the company differs from many others in the sector. The games are often built around multiplayer and communities. A game can look quieter in the statistics for a period only to still have a strong core that comes back to life when a new update drops.

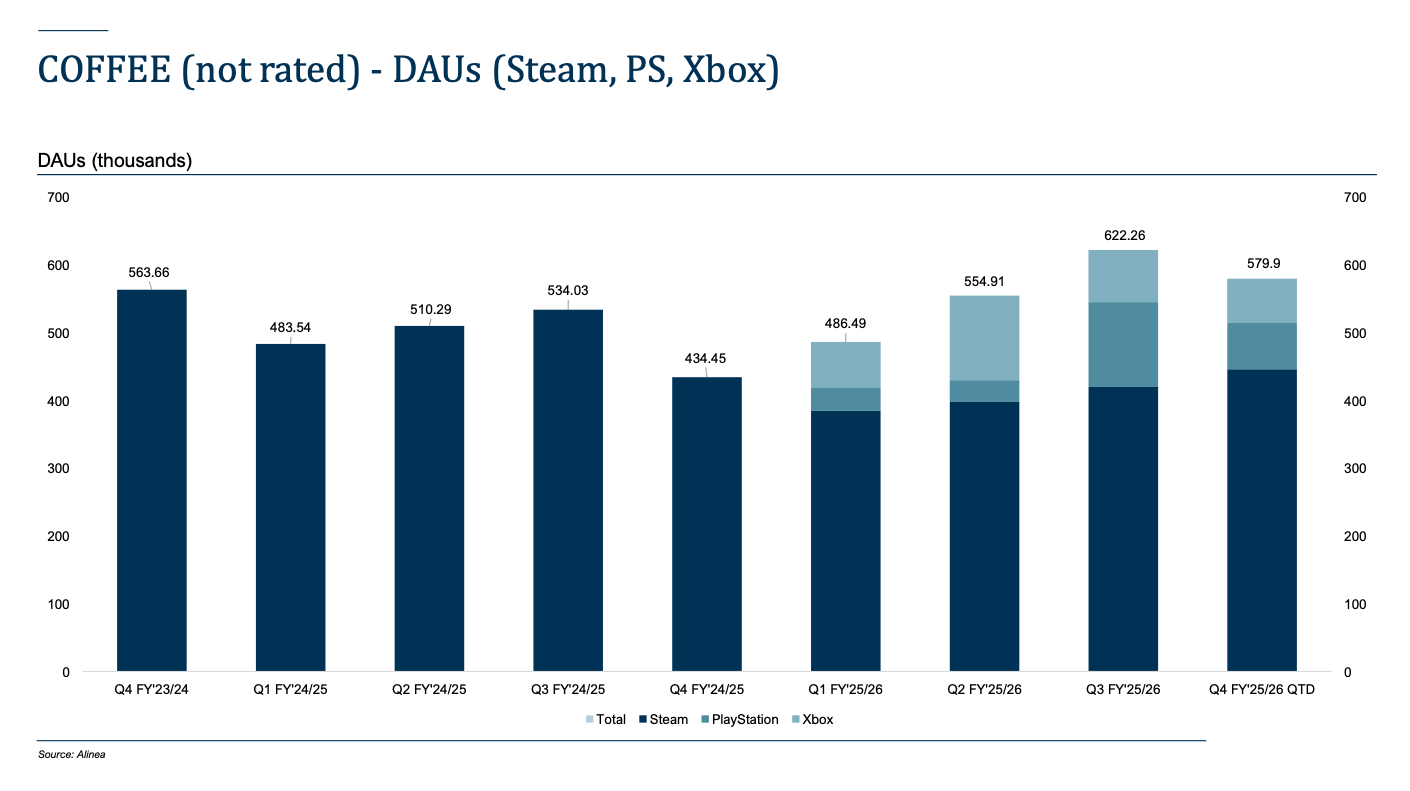

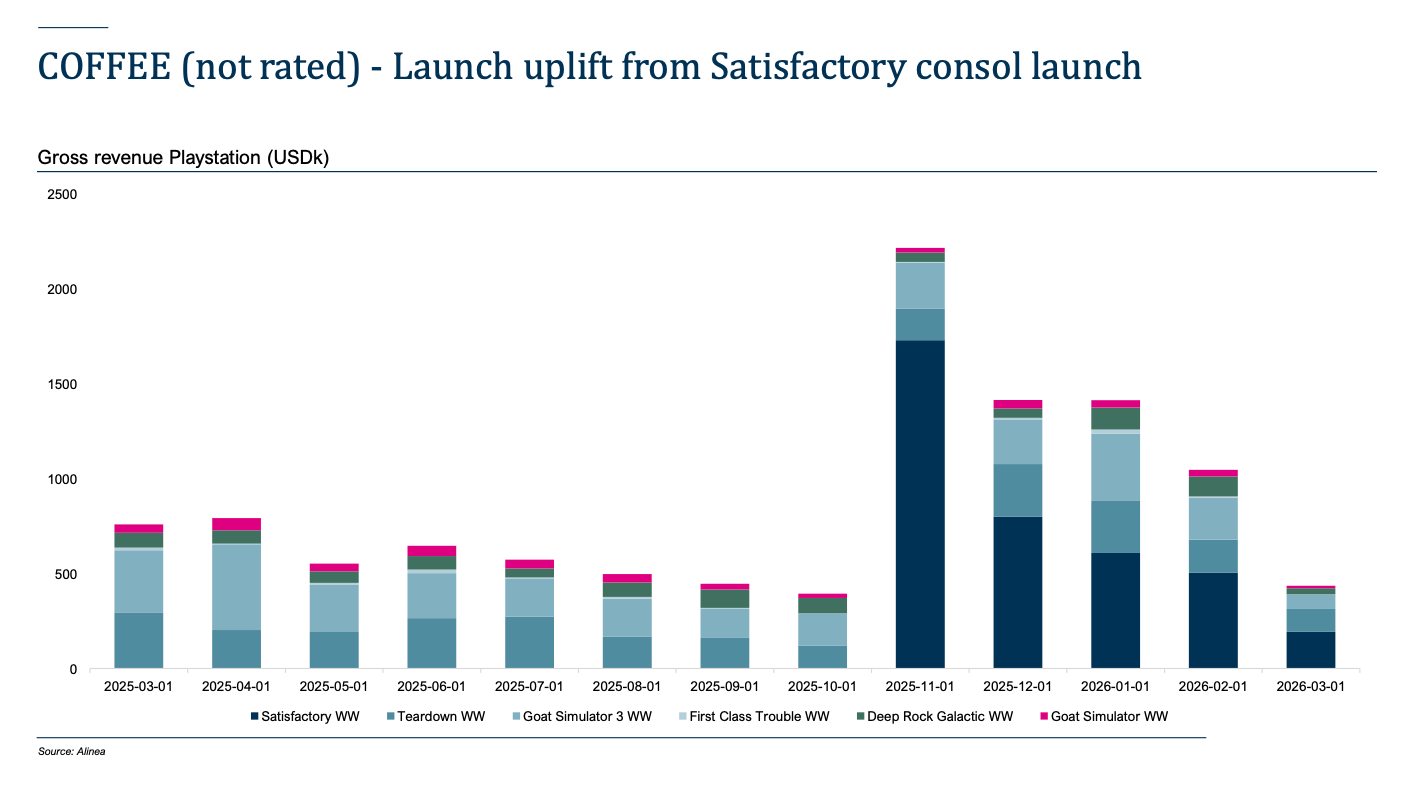

The question of how long-lived the games are isn’t as simple as looking at only Steam either. They’re also expanding games beyond PC as is seen with Satisfactory which recently launched on console, and the developers announced on social media that the targets they had set on a two-year horizon were already achieved in the first quarter after launch.

Furthermore, Valheim is expected to come to PlayStation and Switch 2 during 2026. That console is an important platform for understanding the full puzzle is evident not least when you look at Goat Simulator. That was the game that put Coffee Stain on the map, a sandbox game built on chaos and viral power. Looking at Steam alone, the picture isn’t exactly exhilarating. The CCU peak sits at a meagre 3,500 and sales on the platform are estimated between half a million and a million copies. In context, low numbers to justify having a studio of 31 people working on the IP. But here too many go wrong when analysing Coffee Stain, since the game has a strong foothold on console including several so-called “platform deals”, one of which we saw last quarter.

The simplified Paradox filter

As mentioned, it’s easy to understand why Coffee Stain is often compared with Paradox. Both build on games that live long and can be monetised over time. But that’s also where much of the similarity ends.

Paradox has a different audience and by extension a different economic logic. The centre of gravity lies in complex single-player games with high barriers, a steep learning curve, and an audience that accepts spending both a lot of time and a lot of money on expansions. Coffee Stain has more often built around multiplayer and games that live through the interplay between players, where some leave but many new ones come in with friends. It might sound like a nuance but it’s in practice a major difference in how the games are monetised and how the relationship with players looks over time.

On monetisation specifically, Paradox has pushed their model harder. Expansions and add-ons are released frequently, at a high price. They’ve been able to charge a premium from an audience with unusually high pain tolerance for pricing for a long time. Call it pricing power, which doesn’t come free. When prices go up at the same time as the content is perceived as increasingly thin, friction emerges. This has been visible in the reception of a large portion of the company’s expansions in recent years. What on paper looks like strong monetisation can in the next step erode trust among the most loyal players.

Coffee Stain has chosen a more cautious path. Less out of free will than pure necessity, perhaps. In the type of multiplayer games they tend towards, it’s harder to charge separately for new content without splitting the player base. So it becomes a trade-off you have to make to keep the games alive, with the social networks intact. Rather than squeezing every new piece of content as hard as possible. Incremental earnings are instead sought through game sequels, cosmetics, supporter packs, and keeping the games relevant long enough to bring in new players over time as new discounts and updates arrive. This perhaps less aggressive model gives Coffee Stain significantly higher review scores than the more demanding players at Paradox. Maybe it’s the perception that one sells energy drinks while the other sells heroin?

This is also where Paradox looks comparatively more vulnerable today. A model with high pricing power works best when the player base is growing, or at least when new releases clearly lift activity and earnings. There are signs that the tailwind from COVID and hits like Hearts of Iron and Crusader Kings is no longer as strong. Player base growth doesn’t appear to have grown over the past two years despite several new core titles being added, beyond isolated spikes at launches and so-called “free weekends”. The price increases they’ve had to push through over the past two years have therefore increasingly looked like a way of paying the collection notice for missing growth from shareholders.

This illustrates a more structural problem with Paradox’s aggressive monetisation and expansion model. New sequels are almost inevitably launched in the shadow of their predecessors. Which, after years of expansions, have accumulated a depth and breadth that the new ones lack. Even a fundamentally good new game therefore risks feeling thin next to the old one. For players, the switch isn’t obvious, and for the company it means that the expected incremental boost in activity and earnings that the market likes to count on doesn’t materialise.

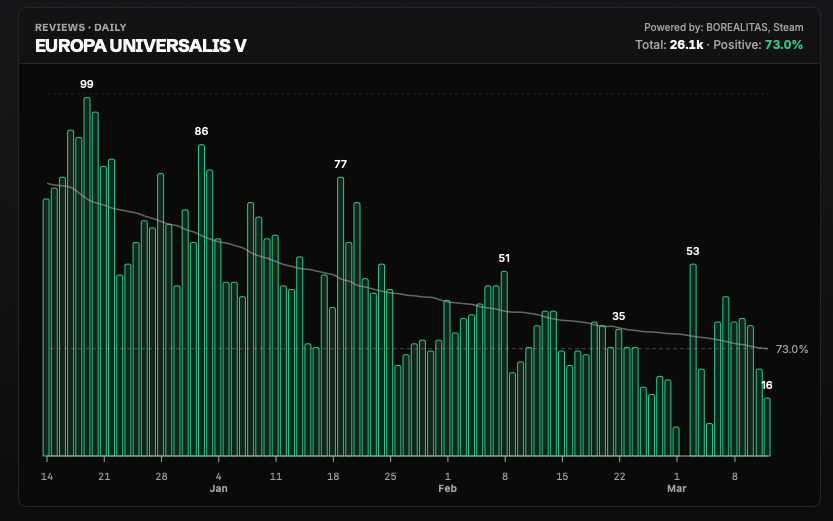

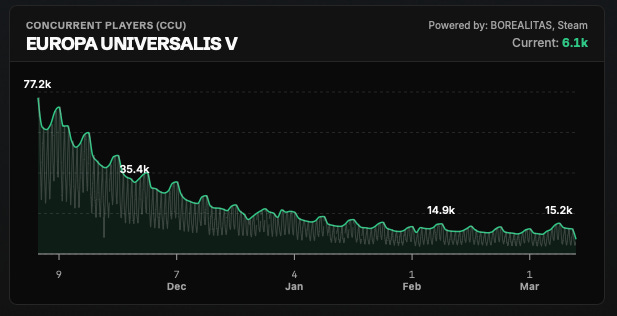

This has shown up in several concrete examples. With Cities: Skylines II it became clear how high expectations can quickly turn to disappointment when delivery falters. The game has wrestled with the same player numbers as its predecessor and the console port has dragged out nearly 3 years. Victoria 3 didn’t become a quick path to profitability either despite a popular IP. Especially not if you factor in costs for continued work on expansions and support after release. On expansions specifically, I estimate that today’s Paradox spends roughly 50% of its development costs, which also demands a significant price tag from players, and that’s where the bulk of earnings come from. Europa Universalis V, which came out this year, was supposed to be the company’s next magnum opus. But has instead sold significantly weaker than analysts expected and met criticism from players that updates so far don’t appear to have turned around. Quite the opposite.

It’s really the same problem recurring in different shapes. Paradox has been able to charge well from its audience, but gives back some of that strength by failing to develop sequels or new titles that feel convincing given its tough target audience. Despite promises to focus on the strategic core from Fredrik Wester since he returned as CEO in 2022. Add to that significant write-downs and impairments on projects over the past four years of Wester’s tenure amounting to around SEK 1.2 billion, what appears from the outside as a model that has tried to chase growth by all means. New games need to be rich enough to motivate a real shift in time, attention, and habit. The number of players and their time is a harder constraint than many calculations want to acknowledge when similar games in the genre cannibalise each other. More DLCs or more titles don’t create more hours from the same audience.

For Coffee Stain’s part, the game is almost a platform and the multiplayer experience a central component. They become less dependent on new titles needing to carry into a new phase of activity. That doesn’t make one model better than the other in any absolute sense. It makes them different. There’s therefore a risk that if you look at Coffee Stain through a simplified Paradox filter, you misunderstand the earnings, the risks, and the robustness over time.

The next growth phase

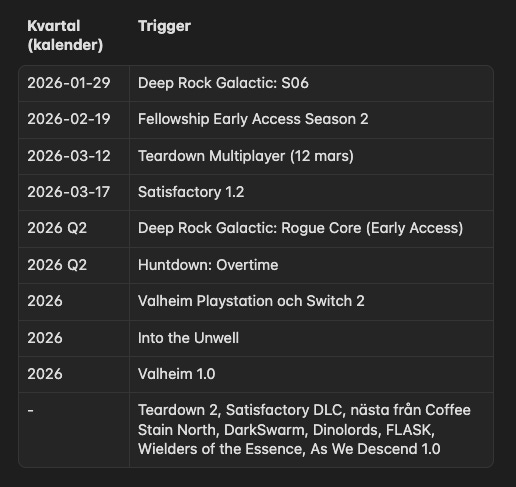

In the current quarter the pipeline is somewhat thinner than the previous one, which beat analyst expectations, but not empty. Deep Rock Galactic: S06 has been released alongside Teardown Multiplayer. At the same time, Satisfactory 1.2 is expected to hit the developer branch next week. Less sequential pressure but should still be enough to avoid negative growth versus last year despite weaker currency. That would be important not least optically. Because then the company can enter stronger coming quarters with a bottom behind it rather than a continued declining curve where the market keeps pushing the inflection point further out.

On a slightly longer horizon, Deep Rock Galactic: Rogue Core is the clearest trigger. The company was expected to announce a launch date on March 12 and expectations lean toward a launch during Q2 this year. The game has been shown in several playtests and streams recently, which have been received very well with review scores above 95%.

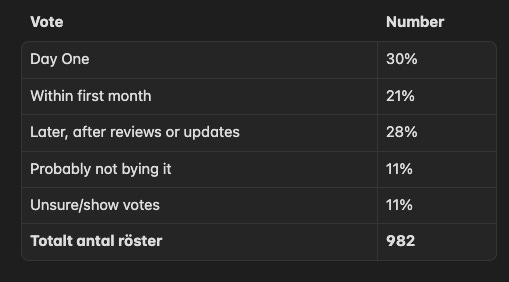

There are also signs that the core audience has received Rogue Core relatively well, despite it deviating from the usual Deep Rock formula by being a roguelite and being somewhat less forgiving. In a poll on the Deep Rock Galactic subreddit, just over half of respondents said they planned to buy the game on day one or within the first month. That shouldn’t be over-interpreted since such polls mainly capture the most engaged part of the player base. But the outcome is still sufficiently indicative that the game doesn’t appear to have hit any obvious red flags with fans. This is relevant particularly given that the original, according to Gamalytic estimates, has 14–16 million owners on Steam. In other words, there’s a large natural audience to work with. The market is probably also underestimating that this could broaden the player base and drive increased earnings since “roguelites” attract a partially new player base, provided they simultaneously let Invisible Walls handle expansions for DRG.

After that comes Valheim, where the expansion to PlayStation and Switch 2 becomes important. Console broadens the player base both organically and through better conditions for cross-play. This is also particularly relevant since the Early Access model as a rule has significantly worse visibility and weaker distribution on console than on PC, something I think is underestimated by the market. When Valheim later this year is expected to reach version 1.0, there are therefore conditions for a clear uplift in both player count and price, if Satisfactory’s 1.0 launch is any guide.

Alongside this, there’s additional optionality from Coffee Stain North, which has now cleared the development costs off the balance sheet after the recent Goat releases, while the studio hasn’t yet announced what the next project will be. That at least opens the door for speculation about a new major title or possibly a sequel.

Satisfactory is another important case in itself. According to statements from the game’s community manager, there are plans for paid expansions. If that becomes reality, the profitability of the title could change meaningfully, since the game already has an established player base and therefore a different monetisation profile than at the initial release.

Fellowship launched with a strong start in Early Access this past winter with over 40 thousand concurrent players on Steam. Since then the picture has cooled considerably and instead turned into a wet blanket. The second season only managed 15 thousand CCU, which raises questions about how strong the reactivation actually is given the game is in Early Access. The base case in the market is that the game won’t lift to 1.0. To give an example of other games that depend on new seasons, Path of Exile had about 300 thousand concurrent players in December, which has fallen to 10 thousand now three months later. Given the outcome from the second season, Coffee Stain currently appears to be losing around SEK 3 million per quarter on the game, which should dampen any concern that Coffee Stain would be running a big loss. Which still feels attractive for the option value of continuing to develop it for another few quarters to see if there’s potential for a 1.0 release, considering how much cash Coffee Stain is sitting on.

Beyond the bigger items, there’s also a tail of smaller games and projects with option value: Teardown 2.0 based on the company’s voxel engine, Huntdown: Overtime, Into the Unwell, DarkSwarm, As We Descend 1.0, Dinolords, Flask, and Wielders of the Essence. They probably aren’t what individually define the case, but they contribute to growth not standing and falling on a single release. And provide options on larger growth.

Particularly interesting in this group is As We Descend, which like Fellowship has been discounted as a flop due to a minimal player base during its Early Access launch. But when you look under the hood, the game appears to be received incredibly well, and the team, now 5 down from 10 previously, consists of industry veterans from Stunlock and Riot Games. Current development costs run at around SEK 40 million, and the expectation is roughly another year of development. The incentives are also there, as 30% of the studio developing it is owned by the CEO of Box Dragon, with the rest by Coffee Stain.

Valuation

With relatively conservative assumptions for the coming twelve months built on roughly 150 thousand copies from Teardown Multiplayer, 500 thousand from Rogue Core, 1 million from Valheim, and 300 thousand from Into the Unwell sold in their respective launch quarters. While the rest of the catalogue is assumed to be largely unchanged, the forecast points to SEK 400 to 450 million in Cash EBIT, with consensus around SEK 440 million. This can be compared to a floor level of roughly SEK 300 million and a consensus of about SEK 330 million for full-year 2025. With an enterprise value of approximately SEK 3.1 billion at around SEK 16.6 share price plus minor adjustments for earn-outs and leases, that means it trades at 7–8x next year’s Cash EBIT. Compared to approximately 9–10x the current year forecast with one unknown quarter.

The difficult part of valuing Coffee Stain is partly the limited history as a listed company, partly the lack of clean comparables. Mobile gaming companies trade today on multiples that in several cases sit close to where Coffee Stain is valued. Despite mobile gaming companies having uncertain revenue durability, worse regulatory predictability, and in many cases weaker cash conversion. At the other end sits Paradox Interactive, which despite expected flat cash flow growth in coming years trades around 24x next year’s cash flow. A valuation that can be seen as high given the nominal cash flow is expected to come in line with Coffee Stain’s for next year.

The most conservative re-rating case probably requires the company to first show actual bottom-line growth. When the market gets increased visibility within roughly two quarters confirming that the player base is more durable than today’s valuation implies, a re-rating towards around 15x cash flow should be a realistic target over time. Should individual game releases or updates also beat expectations, there’s room for additional short-term multiple expansion. It’s therefore not unreasonable to view Coffee Stain as a stock that already today offers a high single-digit and possibly double-digit cash flow yield with free optionality on future growth from new hits.

The market seems to worry today that any growth in the coming year will quickly be followed by declining catalogue sales, and that the company thereafter lacks new projects that can take over. This could potentially be helped by financial guidance from the company’s side. But as long as the catalogue doesn’t show clear signs of accelerating downward and the bigger games aren’t losing players on a larger scale, there’s a relatively limited downside on a short to medium-term basis from a fundamental standpoint relative to the upside in a more positive sentiment environment.

This text does not constitute investment advice and should not be interpreted as a buy or sell recommendation. The author may hold a position in the mentioned securities at the date of publication and at any time. All information is based on publicly available sources and personal assessments. The reader is encouraged to conduct their own analysis before any investment decisions are made.